November 27th, 2020

What Does The Chancellor’s 2020 Spending Review Mean For You?

Chancellor Rishi Sunak delivered the spending review on Wednesday in the midst of the pandemic, announcing changes affecting economic growth, business development and the public sector.

The Chancellor says the government is spending £280bn to get the country through COVID-19. It is important to note that given the uncertainty caused by the pandemic, this year’s spending review covered plans for only one year, in comparison to the usual five-year plan.

CMME explains some of the key points of the spending review and what they mean for you as a self-employed professional (and your mortgage plans) looking ahead.

![]()

‘Long Term Scarring’

Chancellor Sunak says it will take until the end of 2022 for the economy to return to Pre-COVID size, detailing what Sunak calls ‘Long term scarring’.

For the mortgage market, however, 2020 has seen a stimulated and active environment – between house prices rising to record highs, what some are calling a ‘mini’ market boom and the Stamp Duty holiday – the mortgage market hasn’t seen as much of a downfall as other business areas, despite March’s lockdown.

Whilst Sunak noted that “Our economic emergency has only just begun”, many have felt the impact of 2020 already. Check out our recent article on How to Make sense of the Mortgage Market for help navigating the year as it draws to a close.

![]()

The Effect on Businesses?

With the Chancellor’s decision to limit public sector pay rises many have expressed concerns about the effect this will ultimately have on other areas such as small businesses.

Labour MP, Anneliese Dodds – the Shadow Chancellor of the Exchequer, anticipates that the Chancellor’s decision to limit pay rises in the public sector will hit UK businesses: “Firefighters, police officers and teachers will know their spending power is going down so they will spend less in our small businesses and on our high streets”.

David Beaumont, regional director for the South West at Lloyds Bank Commercial Banking, argued however that the plan represented a “Glimmer of hope for businesses” as a result of the Chancellor’s National Infrastructure Strategy.

![]()

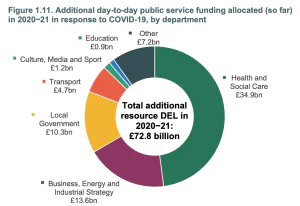

Additional Resources Allocated Day-to-Day Public Services

The total additional funding allocated within the spending review so far in 2020-21 have amassed £72.8billion, the breakdown is as follows:

- Health & Social Care £32.9bn

- Business, Energy & Industrial Strategy £13.6bn

- Local Government £10.3bn

- Transport £4.7bn

- Culture, Media & Sport £1.2bn

- Education £0.9bn

- Other £7.2bn

According to the Institute for Fiscal Studies, 2020.

![]()

Billions in Savings For Taxpayers?

The Chancellor also outlined that the UK will be ending the use of the Retail Prices Index in 2030. This is a decision that will reportedly save billions for the taxpayer but will potentially cut pay-outs to some pensioners.

The Retail Prices Index is a measure of inflation published monthly by the Office for National Statistics. It measures the change in the cost of a representative sample of retail goods and services

This swap means that from 2030, more than 10 million people with traditional final salary pensions will see the annual uprating of their benefits in line with the lower consumer prices index including housing costs.

![]()

Potential For a Rise in Taxes?

Inevitably, with the spending review – particularly this year – spending increases have happened and are expected to continue as the pandemic remains present. Spending increases typically mean tax rises to follow.

Taxes, experts predict, are likely to see an eventual, if delayed, upward trajectory as a result of the Chancellor’s plan as outlined within the spending review.

IR35 & Your Taxes

It’s worth noting as contractors that your relationship with tax may differ from those in standard employment as a result of IR35.

IR35 as defined by HMRC means off-payroll working; ultimately, the legislation is designed to make sure workers are taxed fairly and to identify contractors and businesses which are avoiding paying the appropriate level of tax.

Inside & Outside of IR35

If you operate ‘Inside’ of IR35 you must pay the same tax as an employee, ‘outside’ of IR35 does not make you tax-exempt, however, you can pay yourself a salary and withdraw further income from dividends.

Ahead of the changes in IR35, which were deferred a year, to 6 April 2021. These changes mean that IR35 within the private sector will be aligned with public sector IR35 rules.

![]()

Contractors & Their Mortgage Plans

Stamp Duty Holiday Deadline

The changes announced to Stamp Duty by chancellor Rishi Sunak in July mean that you could still save thousands of pounds on your house purchase – depending upon the percentage of tax that would, ordinarily, be due based on the value of the property you intend to purchase.

There is, until the end of March 2021, a Stamp Duty exemption on properties up to £500,000 and considerable savings above this threshold.

With the market as stimulated as it is, the processing time for mortgage completion can take up to 115 days at the present according to recent market research.

On this basis, your last opportunity to take advantage of the stamp duty savings theoretically sits at the 6th December 2020.

As many home buyers may still have plans to utilise the Stamp Duty holiday an influx may be expected in mortgage applications ahead of this deadline causing potential delays.

To be certain that you will be able to make the most of these savings we recommend beginning your mortgage process as soon as you are ready.

To find out more about the Stamp Duty holiday, see the official government website.

![]()

Is Now the Right Time To Remortgage?

It’s worth remembering that this could be a prime opportunity to look at property investment and remortgage, really 2020 presents a unique chance to explore the avenues for your property plans, maximising your available choices.

As 2020 has seen house prices rising at a rapid rate, your house could be worth more than it was when you set your current mortgage deal. If that’s the case you may find you’re now in a lower loan-to-value (LTV) band, this means you could be eligible for much lower rates.

Try our Remortgage Savings Calculator to see how much you could save!

![]()

Streamline Your Mortgage Plans:

1. Check Your Credit Health

Look at your profile/report to ensure you have a healthy score. Close credit and store cards that you do not use to boost your score, as mortgage lenders treat unused but open credit as potential debt.

Do not undertake credit searches before you look at mortgages. Pay off as much debt as possible.

Use a service like Credit Karma to keep an eye on your credit health.

2. Investigate The Market

Know what house prices are doing and investigate all costs associated with the property including council tax, insurance, and utility bills.

3. Organise Your Paperwork

You will typically need three months’ personal and business bank statements, in-date passport and/or a driving licence, proof of your earnings (contracts or trading accounts if you don’t work via contracts) and proof of deposit.

Check out what our experts about deposits and documents: here’s what they had to say.

4. Get A Deposit

Either save or get a gift from direct family. Generally speaking, the bigger the deposit, the lower the interest rate.

Here are the top seven savings tips for self-employed professionals from CMME: find out how to get better at saving here.

5. Speak To A Specialist Mortgage Broker (Like Us)

Working for yourself takes an independent spirit. CMME understand that and share it.

CMME are proudly independent, meaning they’re free to find the right lending partner for you, to negotiate hard on your behalf and cut a deal that works.

![]()

Useful Resources

- CMME’s Free Guide to Remortgage

- How To Beat The Stamp Duty Holiday Deadline

- Why This Tax Year End Could Be The Most Important Ever

Whether you want to talk specifics or are just after some general advice, CMME can help. Speak to us today on 01489 223 750 for a completely free, no-obligation mortgage consultation. Or click the button below.