July 29th, 2021

Getting the best mortgage rate for contractors can be a daunting prospect. Recent research revealed that only 29% of self-employed homeowners believe mortgage lenders fully understood their earning capabilities when they applied – what effect does this kind of bias in the market have for contractors? It can result in:

- Reduced borrowing potential

- Higher mortgage rates

- Asked for heaps of paperwork

Getting an excellent rate in the first place or making sure you’re on the best one for an existing mortgage can be hassle enough if you’re in traditional employment but contractors may face additional hurdles. CMME explains how you can get the best mortgage rate now.

What’s in the Blog?

- The Basics: Mortgage Rates

- Working out Your Income for a Contractor Mortgage

- How do I Determine my Role?

- Remortgage for Contractors

- Best Rates Currently

- Raising Additional Funds

- Best Times to Remortgage

- Useful Resources

The Basics: Mortgage Rates

Let’s talk about mortgage rates, right from the basics because let’s face it, your main priorities when you’re looking at a new property are normally going to be getting through the mortgage application as quickly as possible and getting a good deal.

Rates are not the thing you’re excited about when you’re thinking about a mortgage, especially as they are only one aspect of obtaining a mortgage as a contractor.

Why? It might seem evident but the better your mortgage rate, the less money you waste every month unnecessarily (if you’d wanted to waste money you would’ve stuck to renting or move on to an SVR with your current mortgage). When you arrange your mortgage, you take the opportunity to shop for the best rate because you – a contractor, a self-employed professional, an entrepreneurial spirit – care about your money.

That’s why when your initial fixed-rate runs out you don’t let that rate roll over onto your lender’s Standard Variable Rate, you’re too smart for that.

Mortgage rates are impacted and influenced by the Bank of England’s base rate which helpfully for all those seeking the best contractor mortgage rate was slashed in March 2020 as an emergency response to the Coronavirus pandemic. It’s remained at that historic low ever since and for you, it means two things:

1. Borrowing is more affordable

2. Savings rates aren’t the most favourable at present.

There’s probably a complex economists’ way of explaining this but in short, the Government sets a goal for inflation and the Bank of England’s Monetary Policy Committee vote on whether to raise or lower the Bank Rate to support this goal. As of July 2021, the inflation goal sits at 2.0% (though the actual rate sits higher than this at 2.3%) and the Bank Rate to support that goal remains at 0.1%.

When it comes to your mortgage that means that right now your initial introductory offer will likely be favourable whether this is your first mortgage or your remortgaging and it means that now may be a good time to check you’re not sat on an unfavourable Standard Variable Rate.

Breaking down your options (Provided for illustrative purposes only)

Say the offer you’re on begins with an Initial Rate fixed for the first 2 years: 0.94%

After these two years, you will automatically move onto the Lender’s Standard Variable Rate: 3.54%

You don’t have to be a math’s prodigy to estimate based on those two rates alone that your monthly payments will be significantly higher on the second rate

The mortgage amount: £350,000

The loan length: 25 years in total

On your initial rate, your monthly repayments are: £1309.57

On your lender’s standard variable rate your monthly repayments go up to: £1855.43

That’s an extra = £545.86 a month or £6550.32 a year – needlessly, because you could potentially remortgage to a better rate.

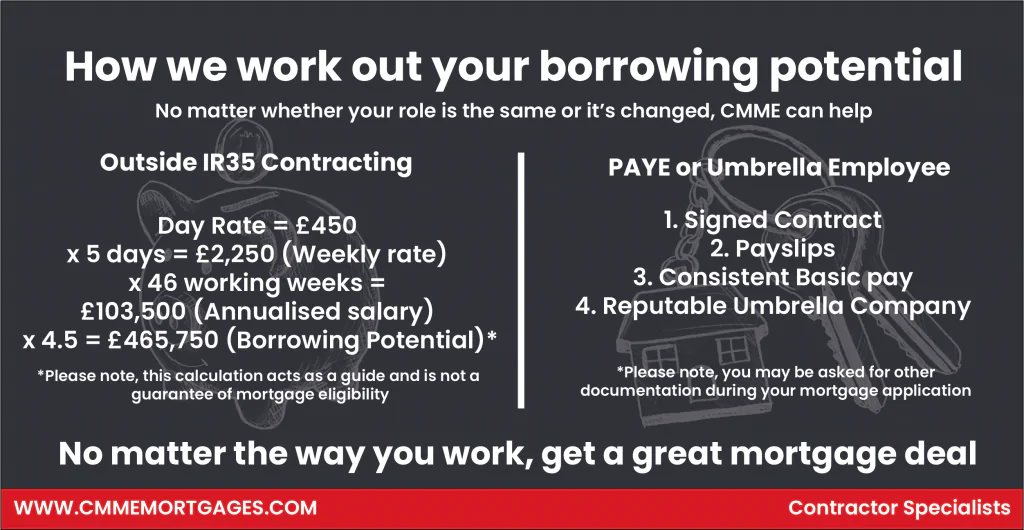

Working out Your Income for a Contractor Mortgage

There are a number of ways you, as a contractor, may want to calculate your income to work out your overall borrowing potential:

- Hourly Rate

- Daily Rate

- Annualised Salary

To calculate any of the above simply follow the formula below:

Hourly Rate x Working hours, per day = Daily Rate

Daily Rate x 260 days (working days) = Annualised Salary (Before tax)

How do I Determine my Role?

With the recent implementation of the changes to IR35, you may have some confusion when it comes to your mortgage application and determining your current role. You may be classified as:

- Umbrella employee

- Umbrella Contractor

- Self-employed

- PAYE

- Contractor

- Ltd. Company

Whilst you might face bias in any of these roles if you approach a high street lender, no matter the way you work or if you have switched from one payment vehicle to another.

Issues you may face as a contractor

In our 2020 research on self-employed homeownership with IPSE, we found that 96% of respondents had to provide more paperwork when applying for their mortgage because they were self-employed.

These market biases are part of the reason it can be worthwhile for contractors to consider a specialist mortgage broker like CMME were using a bespoke process means that we can not only help you to raise the borrowing you require for a mortgage, but it also provides you with access to high street lenders and therefore gives you the range of low-level interest rates that would normally be unavailable when looking at a PAYE contractor mortgage.

Try our mortgage calculator here to see how much you could borrow or our remortgage savings calculator here to see how much you could save.

Remortgage for Contractors

Reasons to consider remortgage:

1. Save money

2. Prioritise your wants, needs and goals

3. Leave a legacy, not a debt

Reasons to not consider remortgage:

1. You just secured a new deal

2. You are concerned about early exit fees

It’s important to know that many people let early exit fees stop them from getting the best deal available – whilst exit fees are something you should consider before changing deals, it is frequently the case that the associated savings with your new mortgage rate could be worth accounting for the early exit fees.

Best Rates Currently

We work with the UK’s leading contractor mortgage lenders to bring contractors more choice and better value.

| Provider | Product Type | Initial Rate | Rate Ends | Cost for Comparison | Lender’s Standard Variable Rate | Redemption Period |

| Halifax | First Time Buyer | 0.87% | 31/12/2023 | 3.2% | 3.59% | 31/12/2023 |

| Coventry Building Society | Offset | 1.35% | 30/09/2023 | 3.9% | 4.49% | 30/09/2023 |

| The Mortgage Works | Buy to Let | 1.19% | 30/09/2023 | 4.5% | 4.74% | 30/09/2023 |

| Virgin Money | Next Time Buyer | 0.94% | 1/12/2023 | 3.8% | 4.34% | 1/12/2023 |

| Progressive Building Society | Discount | 0.99% | 2 years | 3.9% | 4.35% | 2 years |

| NatWest | Tracker | 1.00% | 30/11/2023 | 3.2% | 3.59% | 30/11/2023 |

Rates accurate as of 17/08/21

Exclusive rates are also available from CMME, please contact one of our brokers to discuss further on 01489 223 762.

Best Times to Remortgage

There are some prime times you might want to reconsider reviewing your mortgage rate:

It’s due for renewal & you’re about to move on to a Standard Variable Rate

When you can see the end of your current deal on the horizon, it’s a great time to think about remortgage.

When your current rate comes to an end your lender will automatically swap you over to their Standard Variable Rate (SVR) which is more than likely going to be higher than the deal you were on previously.

It’s worth looking at the market because there may well be a better rate out there for you.

Your house has increased in value

With house prices rising at a rapid rate, your house might be worth a lot more than it was when you set your current mortgage deal.

If that’s the case you may find you’re now in a lower Loan to Value (LTV) band, this means you could be eligible for much lower rates.

Important to note:

Many people let early exit fees stop them from getting the best deal available – whilst exit fees are something you should consider before changing deals, it is frequently the case that the associated savings with your new mortgage rate could be worth accounting for the early exit fees.

The base rate is at a historic low

How does the base rate relate to your remortgage plans? In short, it influences all interest rates, whether you’re borrowing or saving. This means that whilst it remains at this record low, you might be able to make significant savings on your mortgage repayments, depending on your existing rate and other factors.

There’s never a bad time to review your rate, that is one of the things your lender is unlikely to tell you. And, when you fix your mortgage rate, it’s easy to let your introductory period end and let your rate roll over onto your lenders Standard Variable Rate and forget about it. Why is this an issue? Because homeowners are wasting thousands of pounds a year on unfavourable Standard Variable Rate.

This is because your initial mortgage rate is usually going to be an introductory offer and your SVR is likely to be significantly higher than this initial rate. A mortgage broker will do this for you and present the right product for you.

With the base rate at its current standing now could be a great time to consider remortgage.

Raising Additional Funds: Is it Possible Through Remortgage?

When you chose your mortgage originally, you made sure it met your needs. The smart question to ask when it is due for renewal is:

- Does it still work for me?

- Could I raise additional funds to pay for that dream kitchen, or the loft conversion, or home office?

- Could the equity consolidate debts elsewhere and make them easier to manage and your financial commitments more comfortable to live with?

- Would the lump sum pay the deposit on a second investment buy to let property?

The pandemic has made a lot of us review our individual circumstances, whether that’s with a view to our working arrangements or our health, added security has been a priority this year.

Releasing additional funds for home improvements is entirely possible through the remortgage process, making your dreams a very achievable reality.

Clients typically raise additional funds for home improvements, a child’s tuition fees or a wedding.

Get our free Remortgage guide for contractors.

Useful Resources

- Base Rate Update: Why Homeowners Should Consider Remortgage | CMME Explains

- Settling Into IR35: The Future for Contractors | CMME

- Housing Bubble: Trouble on the Horizon? | CMME Investigates

Whether you want to talk specifics or are just after some general advice, CMME can help. Speak to us today on 01489 223 750 for a completely free, no-obligation mortgage consultation. Or click the button below.