July 12th, 2021

With the Stamp Duty Holiday extension behind us, many were concerned about the impact of this end date on the housing market; most were asking one question, will this result in a Housing Bubble?

There has been indecision from industry experts on whether the housing market will experience a lull following the end of the Stamp Duty Holiday, with the original artificial deadline making it difficult to predict behaviour beyond this date.

In this article, CMME explores the market as it currently stands from asking prices to sustainability for the future.

What’s in the Blog?

- What Would a Housing Bubble Mean?

- Potential for a Housing Bubble: Asking Prices

- Impact of the Pandemic

- Interest Rates

- Predictions for the Future

- Useful Resources

What Would a Housing Bubble Mean?

A Housing Bubble is where housing prices are driven up by demand, speculation and exuberant spending to the point of collapse. Now, it’s important to state that the UK housing market isn’t looking down the barrel of a gun labelled ‘collapse’ but recent market activity does raise cause for concern.

Typically housing bubbles start with an increase in demand in the face of a reduced or limited supply and it can take some time to recover from.

Factors that may cause a Housing Bubble ‘pop’ include a downturn in the economy, a rise in interest rates, as well as a drop in demand.

Potential for a Housing Bubble: Asking Prices

Though asking prices are typically not a succinct indicator of true house prices, they have the ability to impact and sway demand. According to Nationwide’s House Price Index annual house price growth rose to 13.4% in June 2021, the highest this level has been since November 2004 – 17 years ago. In addition to this, Nationwide also found that house prices were up in June 0.7% month-on-month, after taking into account seasonal factors.

What does this mean and why has it happened?

House prices rose at a record rate because of immense and sudden demand funnelled into a very short period of time; the Stamp Duty Holiday’s first deadline meant that buyers were rushing to take advantage of potential savings and there simply weren’t enough people selling at the time to support this demand.

Though the extension negated the impact that a hard cut off would have this incentive still arguably put pressure on the UK’s housing market.

The imbalance of supply and demand has the potential to destabilise the housing market. Though the market is buoyant and thriving at present, it is something that we should be aware of as a nation.

Impact of the Pandemic

The turbulent period for the housing market began last spring – its initial closure and then the speed bumps of reopening meant that the mortgage market needed a helping hand to get back to usual levels of activity. In order to do that Chancellor Rishi Sunak announced that there would be a short holiday for Stamp Duty Land Tax thresholds for home buyers. Up until this holiday first-time buyers already experienced an exemption, but this incentive expanded that premise and made home buying cheaper and drove many to action their home-buying plans.

As a motivator it definitely worked; the stimulus that the stamp duty holiday gave to the housing market has been seen as a general success, with the value of new mortgage commitments (lending agreed to be advanced in the coming months) announced in June at a significant 15% higher than a year earlier according to the FCA.

However, due to the housing market’s positive stimulus, this also resulted in an increased average house price by an average of 13.4% as detailed in Nationwide’s House Price Index.

Critics are now saying that the initiative may have been detrimental to home buyers.

The shadow housing secretary, Lucy Powell, has accused the government of worsening a housing affordability crisis by implementing the Stamp Duty holiday; ultimately, fuelling a property price boom during the pandemic.

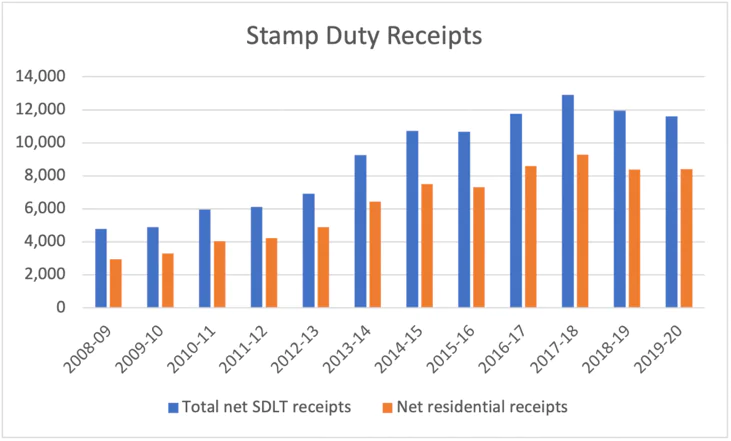

When looking at past numbers of Stamp Duty collected overall and from residential properties, it’s clear that although the holiday introduced was designed for people not to pay the fee, due to the increase in demand and only being available for properties valued below £500k the amount of Stamp Duty paid in 2020 was fairly flat compared to previous 2-year period.

(Source: Gov.uk)

To summarise the impact of the pandemic, the main take away is the implementation of the Stamp Duty Holiday motivated home buyers tempted by savings – for many this meant larger deposits or spare cash. This was arguably juxtaposed to seller intention and now, we’re potentially seeing the results of that imbalance in the market which is driving prices upwards.

How much will Stamp Duty cost you now?

From the Holiday’s initial start in June 2020, buyers haven’t had to pay any Stamp Duty on the first £500,000 of their purchase price.

However, from 1 July, stamp duty will kick in above £250,000 at the following rates:

- £0-£250,000 = 0%

- £250,001-£925,000 = 5%

- £925,001-£1,500,000 = 10%

- £1,500,000+ = 12%

The above is part of a phased return to normal and from 1 October 2021, rates are due to return to normal. That means the point you to start paying stamp duty will revert to the original thresholds:

- £0-£125,000 = 0%

- £125,001-£250,000 = 2%

- £250,001-£925,000 = 5%

- £925,000-£1,500,000 = 10%

- £1,500,000+ = 12%

You can use the government’s Stamp Duty Land Tax (SDLT) calculator to find out how much you would pay.

Interest Rates & Housing Bubbles

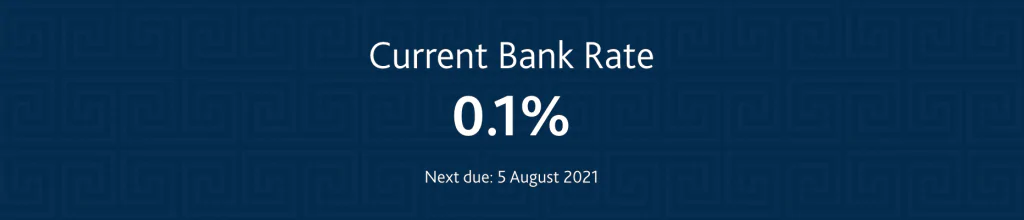

June is the 15th consecutive month with no change to the base rate after its emergency reduction in March 2020 last year – an early response to the pandemic.

Interest rates impact the potential for a Housing Bubble significantly; if we were to see a rise in interest rates it would force the housing market to re-level itself as it were. With inflation rising above the target level, we are unlikely to see interest rates rise in 2021. At least for the time being, the Bank of England’s Monetary Policy Committee has deemed that the interest rate is currently appropriate.

However, this is not necessarily a bad thing. One of the major reasons to take interest in the bank rate is its impact on borrowing and saving, particularly regarding your mortgage plans.

Whilst a housing bubble may concern you if you are already a homeowner you may want to consider your current property before you think about moving.

The bank rate’s historic low means that remortgaging could potentially save you money if you are currently on an unfavourable Standard Variable Rate and this wouldn’t put any additional pressure on the housing market.

Try our Remortgage Calculator & Find out how Much you Could Save

Predictions for the Future

Most are hesitant to make predictions about what the rest of 2021 and the early part of 2022 will look like for the housing market here in the UK, however, there is hope on the horizon.

CMME’s Head of Mortgages, Simon Butler, had this to say:

“After the dust has settled with the end of the stamp duty holiday for homes up to £500,000 it’s likely that we will see a period of reflection. Overall, the market is still active, so the Bank of England need time to consider whether further measures are required.

Early predictions are that house buying will likely remain steady into 2022, which would not be cause for concern. The measure of positivity is likely to be how the sector performs during the summer to autumn months, as this is historically a period in which activity is consistently higher than the winter months.”

Useful Resources

- Base Rate Update: Why Homeowners Should Consider Remortgage | CMME Explains

- Settling Into IR35: The Future for Contractors | CMME

- Industry Update: The Budget, New Products & Your Contractor Mortgage | CMME

Whether you want to talk specifics or are just after some general advice, CMME can help. Speak to us today on 01489 223 750 for a completely free, no-obligation mortgage consultation. Or click the button below.