October 19th, 2020

During these unprecedented times remortgages are becoming more prevalent in the market – around a third of all home loans in the UK are remortgages – but, how does this affect you as a contractor or as an employee of an umbrella company?

Why are we talking about remortgaging now?

You’ve probably heard a lot about the Stamp Duty holiday and house prices rising recently but the mortgage market isn’t only bustling for those looking for new properties.

Remortgages are increasingly common because of the benefits associated with them – remortgaging can be a great way to save you money or free up some cash to use for renovations or to consolidate debts.

What’s more, with the Bank of England base rate is at a historic low and lenders have continued to offer historically low-interest rates in a bid to recapture business lost while the property market was subdued.

What are the reasons to remortgage?

1. Reduce your payments

Your mortgage is probably the largest financial commitment you will ever make, so it makes good business sense to ensure you are on the best rate available before you are moved to your Lender’s Standard Variable Rate.

Don’t just assume you’ve got the best deal. You could reduce your payments by remortgaging – homeowners with unfavourable Standard Variable Rate mortgages are wasting an average of £4,500 a year!

2. Review your life

When you chose your mortgage originally, you made sure it met your needs. The smart question to ask when it is due for renewal is:

- Does it still work for me?

- Could it release equity to pay for that dream kitchen, or the loft conversion, or garden office?

- Could the equity consolidate debts elsewhere and make them easier to manage and your financial commitments more comfortable to live with?

- Would the lump sum pay the deposit on a second property?

COVID-19 has made a lot of us review our individual circumstances, whether that’s with a view to our working arrangements or our health, added security has been a priority this year. Ahead of the changes to IR35 next year, now could be a good time to find the best deal or free up equity.

Equity release is entirely possible through the remortgage process, making your dreams a very achievable reality.

3. Renew your terms

It’s not always about saving money. You can also change the terms on how quickly, or slowly, you pay off your mortgage.

If you’ve recently had an increase in your contract rate, or have inherited some money, you might choose a higher repayment rate and end your mortgage sooner.

This would save you money on the interest paid overall. Conversely, you may want to pay less over a longer term, or a change in job or lifestyle might mean that repayment pauses are necessary.

Finding the right term and flexibility for you would alleviate everyday stresses and offer a reassuring solution.

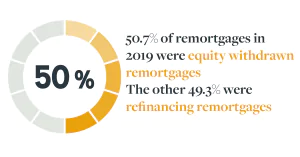

According to Finder, 2020

When should you think about remortgage?

1. You want to take advantage of the low rates

The number one reason you might want to think about remortgaging right now is the historically low base rate set by the Bank of England this year.

The Bank of England base rate affects all loan and mortgage interest rates in the UK. By maintaining the current BoE base rate at 0.1% borrowing is cheaper, but it also means that the returns on savings will be less as well.

Read more about the base rate and what it could mean for you in our recent article: Bank of England Base Rate Stays at 0.1%

2. Your mortgage deal is nearly over

When you can see the end of your current deal on the horizon, it’s a great time to think about remortgage.

When your current rate comes to an end your lender will automatically swap you over to their standard variable rate (SVR) which is more than likely going to be higher than the deal you were on previously.

It’s worth looking at the market because there may well be a better rate out there for you.

3. Your house is worth a lot more than it used to be

With house prices rising at a rapid rate, your house might be worth a lot more than it was when you set your current mortgage deal.

If that’s the case you may find you’re now in a lower loan-to-value (LTV) band, this means you could be eligible for much lower rates.

Important to note:

Many people let early exit fees stop them from getting the best deal available – whilst exit fees are something you should definitely consider before changing deals, it is frequently the case that the associated savings with your new mortgage rate could be worth accounting for the early exit fees.

What happens if you don’t?

Remember, your current lender may not offer the best possible deal for you at the end of your term: the one that lets you reduce your payments, review your life ambitions, or renew your terms.

Ready to see how much you could be saving? Try out our Remortgage Savings Calculator!

Here’s some useful resources that can help you make the most out of remortgage:

CMME can give advice and support to self-employed people and offer bespoke advice on your individual situation. If you would like to know more, contact us today.