October 5th, 2021

Whether you’re an established contractor or you are brand new to the sector it can be difficult to know where you stand with your contractor employment rights.

With the changes to IR35 now firmly in place it’s important that you know exactly what you’re entitled to, the processes you should expect and what you need to look after by yourself.

What’s in the Blog?

- How do you define your role?

- What rights do employees have versus contractors?

- Protecting yourself as a contractor

- Post-IR35 employment rights

- Payments & Evidencing your income

- Useful Resources

How do you define your role?

In the last year, many contractors and self-employed professionals have experienced a shift in their role or how they classify themselves. As contractor specialists, CMME have established processes for facilitating your mortgage application no matter the way you work. Despite this, you may have some confusion when it comes to your mortgage application and determining your current role. You may be classified as:

- Umbrella employee

- Umbrella Contractor

- Self-employed

- PAYE

- Contractor

- Ltd. Company

Whilst you might face bias in any of these roles if you approach a high street lender, no matter the way you work or if you have switched from one payment vehicle to another.

What rights do employees have versus contractors?

According to the government website:

“All employees are workers, but an employee has extra employment rights and responsibilities that don’t apply to workers who aren’t employees. [Like some contractors & self-employed workers]

These rights include all of the rights workers have and:

- Statutory Sick Pay

- statutory maternity, paternity, adoption and shared parental leave and pay (workers only get pay, not leave)

- minimum notice periods if their employment will be ending, for example if an employer is dismissing them

- protection against unfair dismissal

- the right to request flexible working

- time off for emergencies

- Statutory Redundancy Pay

Some of these rights require a minimum length of continuous employment before an employee qualifies for them. An employment contract may state how long this qualification period is.”

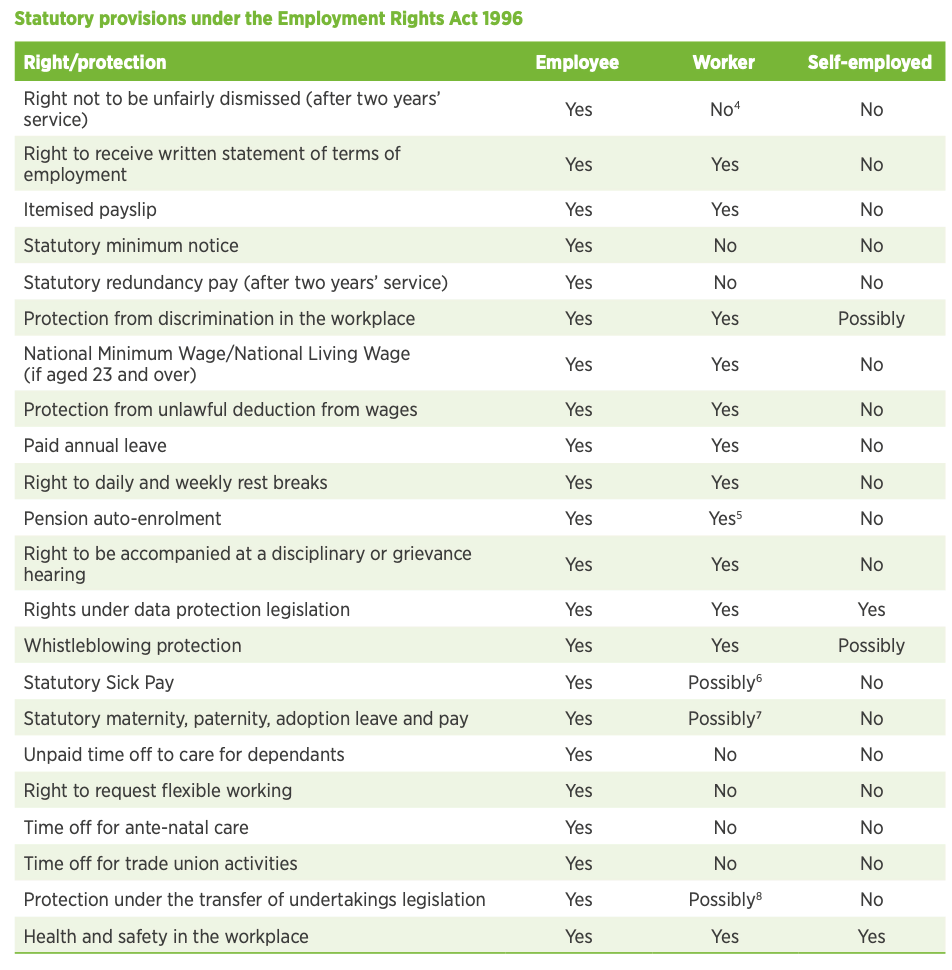

The CIPD (Chartered Institute of Personnel Development) have outlined the rights and protection across classifications, which can be seen below:

Transversely contractors must take responsibility for organise any protection to meet their needs.

Protecting yourself as a contractor

This is a non-exhaustive list of the protections you might consider, however, it’s important to think about what back-up you might want to have in place.

- Income Protection Insurance:

This replaces part of your income if you are unable to work for a long period of time because of illness or disability:

- You can insure up to 60% of your current income (salary and dividends)

- Your take-home payments will be tax-free, as the tax is paid on premiums

- A bespoke plan is built around your unique needs and budget

- Critical Illness Insurance:

This pays out a lump sum if you’re diagnosed with a critical illness. You can use the pay-out for anything such as payments for medical treatment or to pay off your mortgage.

- Life Insurance:

This will ensure your family is taken care of in the unfortunate event of something happening to you.

Post-IR35 employment rights

When you are contracted by a company, what does the process look like now:

Whereas before as a contractor on a day rate you would be hired by a company for services outlined in contract with them and the consideration of tax was primarily your own, now things are different.

You (and the company hiring your services) now need to be aware of whether the work will be identified as either outside or inside IR35 – many companies will have assessments to confirm your IR35 status prior to working for them.

Companies you work with should have ensured that there are written agreements in place for self-employed contractors which reflect the arrangements correctly. It should make your tax status clear and clarify whether the engagement is of a sole trader or a limited company contractor.

Any company you undertake work for should also have an appeals process for contractors who wish to challenge the IR35 determination they are given. If you are unhappy with the determination given following the proper channels of the appeals process, you may be able to reach reasonable adjustments with the company or choose to decline the work if you so wish.

Many companies are seeing more ‘inside’ determinations and contractors should prepare accordingly with options like umbrella companies available to you.

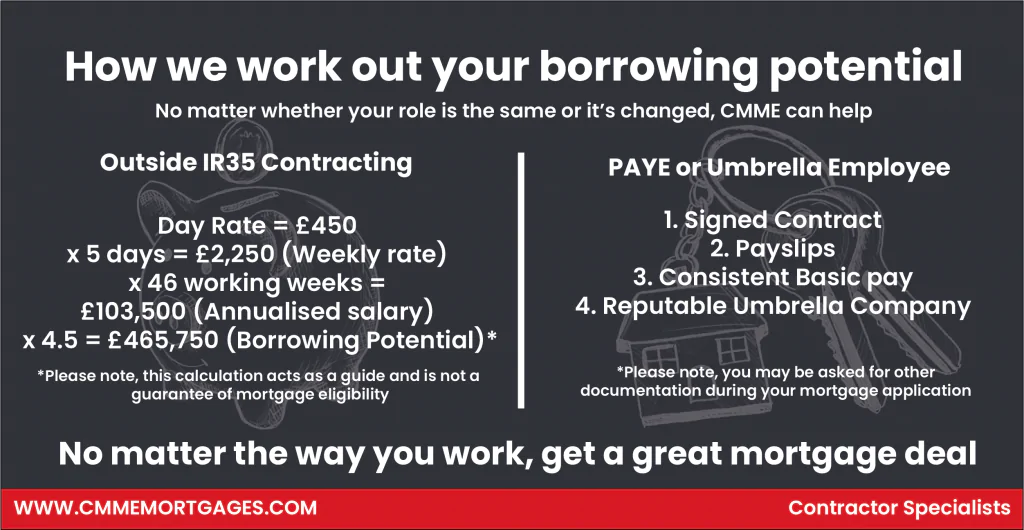

Payments & Evidencing Your Income

The way you’re paid as a self-employed professional or contractor may vary depending on your role classification. For example if you work as an umbrella employee it may vary vastly from an independent freelancer.

There are a number of ways you, as a contractor, may want to calculate your income to work out your overall borrowing potential:

- Hourly Rate

- Daily Rate

- Annualised Salary

To calculate any of the above simply follow the formula below:

Hourly Rate x Working hours, per day = Daily Rate

Daily Rate x 260 days (working days) = Annualised Salary (Before tax)

Useful Resources

- Base Rate Update: Why Homeowners Should Consider Remortgage | CMME Explains

- Settling Into IR35: The Future for Contractors | CMME

- Housing Bubble: Trouble on the Horizon? | CMME Investigates

Whether you want to talk specifics or are just after some general advice, CMME can help. Speak to us today on 01489 223 750 for a completely free, no-obligation mortgage consultation. Or click the button below.