June 22nd, 2021

The extension to the Stamp Duty holiday is due to end this month and it’s leaving those with home purchase plans wondering what this means for their mortgage and for their budget. Crucially, we’re asking what next after the Stamp Duty Holiday extension ends?

In this blog CMME considers everything from: what’s happened with Stamp Duty since 2020 to whether Stamp Duty still serves its function and what this means for your mortgage plans.

What’s in This Blog?

- What’s Happened with Stamp Duty Since 2020?

- The COVID-19 Response

- 2021 Extension

- Moving Forward Stamp Duty Implication

- Should we Scrap the Stamp Duty Land Tax?

- House Prices & Mortgage Activity

- Other Schemes of Note

- Mortgage Tips for 2021

- Useful Resources

What’s Happened with Stamp Duty Since 2020?

The COVID-19 Response

Though it seems like a lifetime ago, it was only last July that the Stamp Duty holiday came into fruition. The change to the Stamp Duty Land Tax threshold was proposed to stimulate the mortgage market after its involuntary standstill in the early part of last year.

Whilst there have been subsequent lockdowns and closures, the market has not felt the force of COVID-19 as significantly as in the initial Coronavirus response back in March 2020.

As a considerable boon to homebuyers the Stamp Duty holiday in its initial form and thereafter in its extension, meant that buyers have been able to benefit from additional savings over the last year which increase exponentially based on the cost of the house.

The stimulus that the Stamp Duty holiday provided to homebuyers propelled the market after the downturn seen regarding home purchases briefly in the early portion of last year, with house purchasing and lending reaching a 6.8% increase compared to the previous year (Source: FCA).

Many home buyers will be disappointed to have missed the Stamp Duty holiday when the tax resumes following the extension, as it is one of the various costs homebuyers ordinarily need to account for (sans first time buyers) and one that can tally up very quickly.

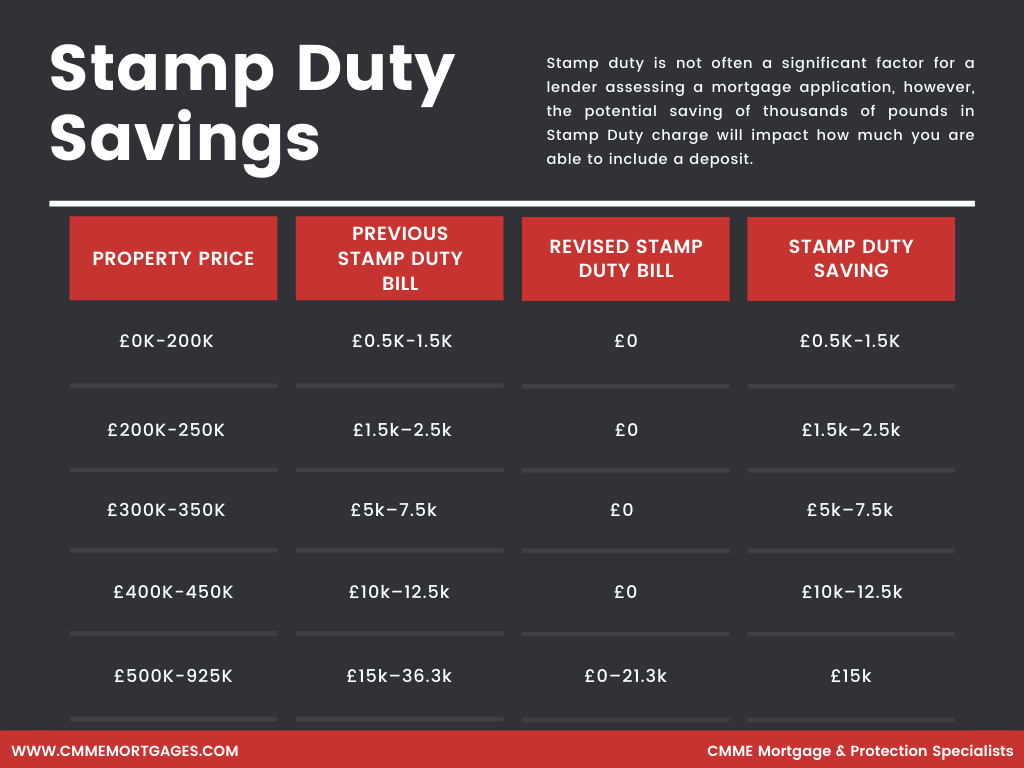

The table below illustrates the potential savings associated with the Stamp Duty holiday until the end of June 2021.

2021 Extension

In March 2021 it was announced in the Spring Budget Review that the Stamp Duty holiday would be extended ahead of its original end date in the same month.

Chancellor Rishi Sunak implemented the extension in order to support the property market after fears that the sharp end to the threshold change would severely impact the market. The economic impact of the lockdown required careful handling to not reverse the boost to the market it had been intended to support; the extension of this tax holiday was an instrumental move for home buyers and the economy alike, costing a reported £1bn for the Treasury to extend (Source: The Times).

Moving Forward Stamp Duty Implication

The threshold savings as outlined above will remain until 30th June 2021 but this is not a hard finish to the Stamp Duty changes unlike the proposed March 2021 end of the original holiday. From 30th June 2021 to 30th September 2021 a staggered exit from the holiday will mean that you do not have to pay any Stamp Duty on a residential property bought for up to £250,000.

The extension in itself and the tapered end mean that even more home buyers have been able to benefit from the huge savings associated with the Stamp Duty holiday – which has ultimately resulted in lots of home buyers being able to increase their budget, getting more house for their money in the long run.

You can read more about Stamp Duty Land Tax on the Government website here.

Should we Scrap the Stamp Duty Land Tax?

This is a debate larger than the holiday and extension itself but one worth considering: does the Stamp Duty Land Tax still serve its purpose?

Forbes wrote back in 2019 that a Stamp Duty reform was required in order to save the UK housing market and there is considerable weight behind critics of the tax; prior to the house prices rising over the course of 2020 into 2021, 2019 saw London house prices falling swiftly in a 12-month succession – the most significant decline in a decade (Source: Property Reporter). Critics and economist pointed to Stamp Duty as a key player in slowing the housing market at this time.

Now, two years on without the Stamp Duty tax (up to £500,000) we’ve seen the market thrive, house prices have risen, and the mortgage market has never been healthier. It’s hard to not see a correlation. Stamp Duty brings in around £12bn a year for the government – about 2% of the tax the treasury collects so it’s unlikely to go anywhere soon (Source: The Times).

There is certainly an argument for removing the tax altogether, replacing it with council tax or the proposed property levy, however a permanent threshold reduction could be an alternative middle ground – and one that many people are calling for (Source: The Times).

House Prices & Mortgage Activity

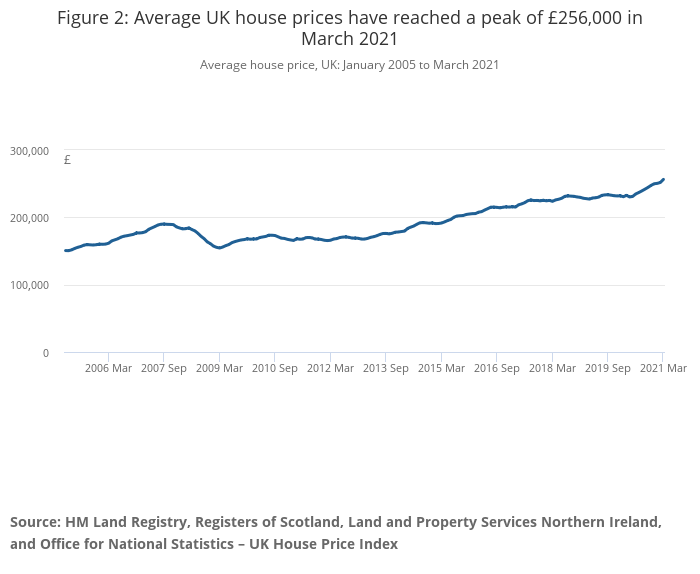

According to the Office of National Statistics, on a non-seasonally adjusted basis, average house prices in the UK increased by 1.8% between February and March 2021, compared with an increase of 0.9% in the same period a year ago (Source: ONS).

It should be noted that while March’s spike in house purchase and prices was potentially driven by the original end date of the Stamp Duty holiday, a lot of momentum has been maintained. Nationwide’s research indicates that the extension to the Stamp Duty holiday is not the key factor, though it has clearly had an impact on the timing of transactions (Source: Nationwide).

In their April 2021 survey Nationwide found that 68% of respondents would have continued with their home moving plans regardless of whether the Stamp Duty holiday had been extended. Instead, they conclude, it is the shift in priorities and preferences for the home that is propelling house purchase activity.

Other Schemes of Note

What other schemes and incentives have the Government announced recently? In a large part, they’re helpful to First Time Buyers, but to summarise:

95% Mortgage Guarantee Scheme

First-time buyers, home movers and previous homeowners with a 5% deposit will be able to access 95% Loan to Value (LTV) mortgages under the new scheme announced in the March budget by Chancellor Rishi Sunak.

The new scheme, similar to the 5% Help to Buy Government scheme that ran 2013-2017, will run from April 2021 – December 2022. The key difference between the ongoing Help to Buy scheme, which is focused on new build property only, is that this provides buyers the opportunity to purchase existing homes with a smaller deposit.

To be eligible for a guarantee under the scheme; the mortgage will need to:

- be a residential mortgage (not second homes) and not buy to let

- be taken out by an individual or individuals rather than an incorporated company

- be on a property in the UK with purchase value of £600,000 or less

- be a repayment mortgage and not interest-only

Read more about the 95% Mortgage Guarantee Scheme here.

The New Help to Buy Scheme 2021-2023

The Help to Buy 2021 – 2023 is a new version of the scheme for first-time buyers and is currently open for new applications. If you qualify, it will allow you to navigate the hurdle of raising a deposit for a property, by giving you a government loan to cover the cost.

The loan needs to be repaid in full, and you may end up paying back more than you borrowed, especially if the property dramatically increases in value and you sell it before you’ve paid the loan back.

And remember, this new scheme is only for First Time Buyer’s wanting to buy a new build property from a registered homebuilder; eligible first-time buyers were able to reserve their homes from mid-December 2020 and get the keys to move in from 1 April 2021.

The new 2021-2023 scheme runs to March 2023.

You can read more about the Help to Buy Scheme here.

5 Tips for Getting Mortgage Ready in 2021

1.Improve your credit score

Here are some quick tips for improving your credit score:

- Register on the electoral roll

- Check for any errors and have them removed

- Pay off existing debt

- Don’t do lots of credit checks

- Pay your bills on time, don’t miss payments

Try an app like Credit Karma for keeping track and finding tips for improving your credit score.

2. Decide on your budget

In light of Coronavirus, many lenders have reduced the availability of high Loan-To-Value (LTV) mortgages meaning that you will often require a higher deposit than you may have previously, somewhere in the 10-15% range is more prevalent than a 5% in the current climate.

Lenders tend to favour individuals who have higher deposits, but this is true to anyone looking for a mortgage and not just contractors.

To access the most competitive rates you should be aiming to save anything between 10 and 25%. There are mortgage options out there for less than that, but they will be on a much higher rate.

We asked our experts everything you need to know about deposits, check it out here.

3. Get your paperwork sorted

You will need to provide minimal documentation to support your application. Ensure your CV is up to date as it will be used to prove your skills and experience.

You will also need to obtain a copy of your current contract as this will be used to demonstrate your earnings. Using these documents, we can avoid any issues to do with affordability.

Our process is a simple as that. We won’t ask you for heaps of documents we might not need, we know the way you work, and we’ll make the process as easy as can be.

We asked our experts everything you need to know about documents, check it out here.

4. Investigate the market

Before you start your mortgage process, it’s a good idea to have a look at the market – investigate what type of mortgage might suit you and your needs, what area would suit you and the costs associated with your new mortgage and property. Ask yourself, after the Stamp Duty Holiday extension ends what will it mean for my current plans?

Whether this is your first mortgage or your fifteenth, preparing in advance can help make sure your goals are realistic and achievable.

5. Speak to a specialist

The truth is that most lenders have little understanding about the contracting market, and as a result, their standardised procedures do not accommodate contractors.

We have agreed bespoke underwriting agreements with a comprehensive range of lenders enabling us to secure mortgage funding based on a multiple of your contract rate alone.

Useful Resources

- Limited Company or Umbrella Company? Which Role Works Best For You | CMME Explains

- So, You’re Thinking About Contractor Buy to Let? | CMME

- Exclusive Mortgage Rates for Contractors | CMME

Whether you want to talk specifics or are just after some general advice, CMME can help. Speak to us today on 01489 223 750 for a completely free, no-obligation mortgage consultation. Or click the button below.